Volatility is low across many asset classes. If volatility is a measure of uncertainty, then this is a bit strange. These seem to be some of the most confusing economic times in recent history, with ever present calls for market crashes while stock markets move up, bonds stay very high, and oil moves sideways.

Central bank policy has provided strength to most markets, as they are designed to do. This has in effect reduced downside volatility. Oil is trading at less than 20% implied volatility, well below historic levels, even as economic uncertainty is high. Oil production in the U.S. is growing and should be putting downward pressure on oil, but prices have been moving sideways since 2011. Why would $100 WTI, with rising supply and economic crashes always around the corner, be trading at <20% implied put side volatility?

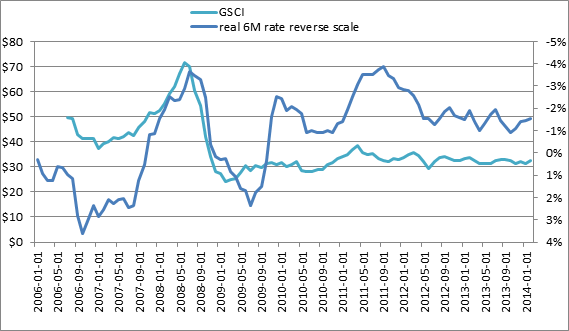

At least part of the answer seems to involve central bank policy. Low interest rates have sent money out to non-traditional markets in search of yield. Commodities like oil benefit from this. Low interest rates also incentivize oil producers to keep oil in the ground. If their option is to put their proceeds from oil sales into low to negative real rate paying treasuries, then why not wait? Lastly, the money used by central banks to buy the bonds that keep interest rates low needs a home. The new money is a wealth transfer from savers to the receivers of the new money, so there is a constant flow of real, not nominal, savings to the bondholders. They will be looking for somewhere to invest the money. These three factors, put in place because of the uncertainty the world faces, have led to the paradox of lower volatility in the face of greater uncertainty.

Below is a chart showing the Goldman Sachs commodity index with real 6 month interest rates: