So says Andrew Smithers in the FT. He’s right. The ability to make economic forecasts is highly dubious from both theoretical and empirical viewpoints. Theoretically, human behavior and interaction is not governed by any stable rules or relationships. This leads to almost infinite combinations of events, and the possible combinations are always changing. Empirically, economists are usually wrong in their forecasts.

It is probably a better idea to focus on positioning oneself with the probable current, not try to guess where that current will take you. In today’s world this usually means trying to understand the likely effects of government, especially central bank, policy on markets. Free markets with free banking would offer weaker and shorter lived currents. Better for average people, but worse for speculators.

Unfortunately, reducing one’s goals to simply being on the right side, probabilistically speaking, is not easy. We are not talking about probability in the sense it is used in the natural sciences. There are no stable distributions in economics. Indeed, the most common distribution used in economics and finance, the normal distribution and its offshoots, is based on coin tossing where the probability of each of two possible outcomes is known and stable. This is not the case when dealing with human beings, whose value scales, tastes, hopes, fears, time preferences, moods, etc. are in constant flux. This means their reactions to events, which are themselves usually the result of other peoples’ reactions, are unstable from a probability standpoint. Gambling probability, from which much of financial probability takes its inspiration, deals with large classes of events governed by the same probabilistic laws. Human behavior, on the other hand, deals with individual cases, each of which has never happened before and which will never happen again, and hence are not governed by any knowable probability distributions. The a priori distributions we put on them in order to understand them sometimes deviate from the results a posteriori. This is the danger.

Another quote from Smithers in the article:

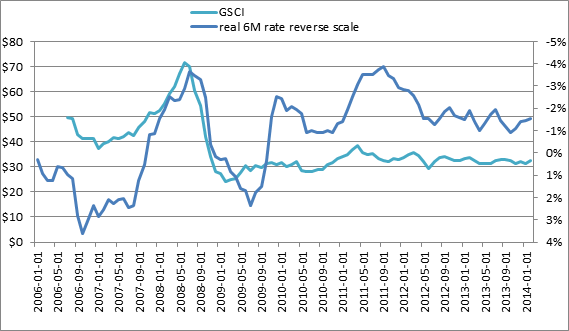

“Prior to the great crash, Ben Bernanke wrote a paper claiming that central bankers have been responsible for what he called the ‘great moderation’. I thought he was right but I thought it was a disaster: in the process of moderating the swings of economies, they were also moderating the perceived riskiness of debt.”

Making economies appear less volatile than they are makes markets riskier. The price stabilizing policies only serve to mask the true price changes, which makes economic calculation more difficult. In this case, debt is underpriced in light of the true risk inherent in the economy. People only see things through a monetary lens. They see and react to nominal prices, not real prices. This is when the miscalculation happens.